The top vendors in the overall storage software market are led by EMC with 24% share in 2008, followed by Symantec at 18%, IBM at 13%, and NetApp at 8%. Interestingly, although these players command substantial presence smaller companies continue to chip away at market share. I would not be surprised if, in ten years, the list of top ten vendors shuffles around quite a bit.

According to IDC, the total data created by businesses and consumers is roughly doubling every 18 months. At this current rate, the universe of content created across the globe will grow five-fold by the end of 2012. And, there’s no clear end in sight. It doesn’t take much to understand this when one starts to think about their own personal storage growth over just a few months. Among others, the obvious following factors are playing a key role in this data deluge:

Global growth in Internet users, broadband penetration, and Internet-connected devices (both in terms of multiple computers per user and, now, powerful mobile devices).

Adoption of social networking applications and the exponential growth in media (photos, video, & music) that gets duplicated & distributed across the network.

Increasing bandwidth availability (which enables richer and bigger applications, especially video).

Migration of content stored on old media (paper, film, etc.) into digital format (movies, music, legal files, letters, books, magazines, etc) and the coming digitization of healthcare and other records.

This increasing deluge of digital data, I believe, is bolstering a continuously growing demand for focused storage software (and services), starting with traditional backup & recovery (with improved functionality across platforms & media), replication, archiving, and storage management.

Another important data point to consider is that today corporate organizations spend, on average, 28% of IT capital expenditures on data storage hardware, software, and services. That’s a massive percent. Given that a large majority of that is hardware today, how will that percent evolve over the next ten years as data continues to grow exponentially and historic data continues to accumulate?

Put into perspective from a consumer angle; think about what your files would look like if you had kept every single photo you ever took, every letter/paper you ever wrote, every card you ever received, every drawing you ever drew, and every document you ever saw or read. Had you kept all of that material/ media for your lifetime, how would you manage it today? How would you go about finding something? How would you decide where to file something?

In this digital age, where we are individually clearly keeping more personal media than we ever have before (just think about the number of digital photos you have on your hard drive versus three years ago), we are individually spending much less, as a percent, than corporations do. Our spending on media & communications has dramatically increased over the past twenty years, but our personal spending on filing & storage of that media has not increased in a corresponding manner.

This material increase in data clearly presents a huge opportunity for continued innovation in capacity optimization technologies and more efficient system architectures to address this massive piece of our IT ecosystem (both in corporate environments and in the consumers’ living room).

Storage is a key component of this wave of digital media innovation we are living in. So, if you ask me, the innovative companies in storage software are going to appear & grow mainly because of:

As mentioned above, absolute growth in bits & bytes, highlighting increased for storage management and protection processes, both for ease of access and for cost reduction.

Cloud computing, which is shifting the physical location of data, and demanding new tools & solutions to deliver storage-as-a-service, archiving & de-duplication, and multi-tenant management.

Increasing platform & application complexity, where we are moving from a singular platform (Microsoft) and a handful of application standards (text, images, email) to multiple platforms and applications.

This last point is critical. A few years ago, we lived a world where we basically backed up Microsoft and, mainly, MS Office applications (along with some basic 2D & 3D media files). Today, storage software has to deal with heterogeneous environments (for instance, various kinds of mobile data devices, networked computers, netbooks, and Apple, gaining ground in the desktop world), and an increasing number of file types & media.

There is clearly a lot of innovation yet to come in an industry that many view as mature.

A few years ago, at some technology conference, I received & read The Singularity is Near by Ray Kurzwell, and all I could think of was Skynet from the film series The Terminator. The book insightfully explores the merging of technology and biology, and its implications for the future. The 672 page tome dives into nerdy augury of the coalescence of genetics, nanotechnology and robotics. As a Blade Runner fan, Kurzweil's predictions of evolution are a scientists wet dream.

Paul Kedrosky recently posted the above trailer and it's gotten me excited to to see the documentary, Transcendent Man. As in the book, Kurzweil argues that artificial intelligence is improving exponentially, and eventually – the latest ETA is apparently 2045 – computing will become self-conscious and "alive". Bring it.

Yesterday, Google introduced its long-awaited touch-screen phone, called the Nexus One. This long-awaited new device/announcement is driving some chatter about the future of the Mobile OS world. Much of the chatter is around pricing (to carriers), revenue model, and market share. Google is effectively paying carriers to sell it's phone (platform) with the intent to generate revenues from search down the road. That's a substantially different approach than Apple took with the iPhone.

Rather than re-hashing all the ins & outs of Apple versus Google, Bill Gurley does a good job here.

But, the question to ponder is whether the market will evolve as Macintosh and Windows did or whether Apple will hold ground & continue to grow. Will, over time, the Mobile OS world sustain multiple providers or will we end up in a world where one OS dominates market share?

Is there a developer, application, and user network effect in the mobile world? Any kind of network effect could impact this outcome uniquely.

On the face of things, it would seem to me that Google is taking a page from the Microsoft Windows playbook and Apple is taking a page from, well, the, uh, not so successful Apple Macintosh playbook.

It could also just be that the Mobile OS world can end up looking very much like the video game console industry, with three players (Microsoft XBox, Sony PlayStation, & Nintendo Wii) today equally vying for market share along with several other players (Sega, Atari, 3DO, NEC, RCA, etc) making waves here & there.

What about RIM, Nokia, Motorola, and Symbian in this above discussion? And, dare I say, Palm? Is it sound to simply assume that these players are out of the running?

Although more free market examples would imply a standard Google & Microsoft analogy, only time will tell how the Mobile OS world evolves differently. As mobile applications become more complex, 3G connectivity becomes more pervasive, and devices become more powerful, the Mobile OS landscape will also become more expensive to compete in. For now, though, my guess is that it's still pretty early to start predicting the next Windows.

Welcome to the future of unlimited ad supply! With the development of digital networks, the internet, and mobile communications, the media industry is faced with a nearly limitless supply of potential advertising inventory. Hmm.... Will the demand curve move up to meet this new supply? Google has demonstrated that it can attract new demand (new advertisers), but how far will it go?

Without getting into details of the Law of Supply and Demand in Economics 101 (something well covered here, as it relates to Google), I think it's worth understanding the impact of abundant supply on the various sectors within the media industry.

The Internet, Schumpeter's latest example of creative destruction, with an unlimited supply of content, broad reach, and (near) perfect performance measurability, has all but crushed the oligopolies that have dominated the media landscape for the past 50+ years. Until the Internet, the primary media outlets were, in order of advertising importance, (a) television, (b) newspapers, (c) radio, (d) billboards, and (e) magazines. And, the way that Madison Avenue determined how to allocate advertising budgets and pricing was (a) sexiness, (b) reach, and (c) measurability. It was simple, television ads are very sexy, can have local or national reach, but have weak measurability. Newspapers present a different reach but are inherently more local. Radio is an auditory experience, therefore more stimulating, but difficult to measure. Billboards can provide local or national audiences and, depending on the target, are more or less measurable. Magazines provide a visual medium with targeted demographics within national distribution, which is great for targeted branding, but difficult to measure.

Then along came the good ol' Internet, which over time continues to provide exponentially better measurability than any of the legacy mediums. And, more importantly, provides better targeting / effectiveness because of the availability (technologically and otherwise) of better consumer data (at a basic level, specific geography, sex, age, and various preferences).

But it's not just the world wide web that's screwed things up! The ad world has been in constant evolution over the past 50 years. The Buggles nailed it in 1981 with their MTV hit, Video Killed the Radio Star. And, now, the digitization of everything has impacted each particular media outlet directly. So, what specifically has happened to the five traditional media outlets over time:

Television. Ever since the proliferation of cable television, we (viewers, advertiser targets) have faced content overload. In addition to basic broadcast television networks (e.g., ABC, CBS, NBC, CW, Fox, PBS) and local-access television channels, there are now hundreds of other specialized and premium channels, all of who survive largely on advertising revenue (although many also receive subscriber fees from the cable operators for, on average, 5-50 cents per subscriber per month. Without that subscription revenue, many of these cable favorites would not survive. So, not only is the ad revenue threatened by the proliferation of media, but so are other revenue streams threatened by disintermediation. Commonplace living room toys such DVRs threaten ads as does streaming internet video, downloaded video files, Hulu, YouTube, DVDs, AppleTV, Netflix, and on-demand directly from the set-top box.

Newspapers. The obvious first to bear the brunt of the impact of the Internet, newspapers aren't completely new to competition. At one point, as the only medium really, newspapers held a dominant role in society ever since the movable type at the beginning of the 17th century. However, newspaper magnates were threatened by the proliferation of their own industry, dailies, weeklies, & monthlies, and then magazines and eventually even radio. Over the past century, newspapers have survived the various competitive threats, mainly because of their strong-hold over local markets to deliver local advertising and the ever growing demand for local advertising. However, by the early 1990s the availability of news via 24-hour television channels posed an ongoing challenge to the business model of most newspapers. Paid circulation declined, and advertising revenue (roughly 80% of most newspapers’ income) followed suit. Less than a decade later, the Internet (led by hundreds of news portals and Craigslist), started to take a big bite out of an already weakened industry.

Radio. The first twenty years of radio thrived in a non-ad supported environment. Many of the first stations that started in the 1920s were owned by manufacturers (for the primary purpose of selling more radios). NBC was started by RCA in 1926. Even once radio stations began relying on advertising revenues, the standard analog television was introduced in the 1940s then color television in the 1960s. Radio barely had time to establish itself as a powerful ad medium before television took the main stage. Interestingly, when radio became more prevalent in the 1930s, many predicted the end of records. Radio was a free medium for the public to hear music for which they would normally pay. Indeed, the music recording industry had a severe drop in profits after the introduction of the radio. For a while, it appeared as though radio was a definite threat to the record industry. Radio ownership grew from 2 out of 5 homes in 1931 to 4 out of 5 homes in 1938. Meanwhile record sales fell from $75 million in 1929 to $26 million in 1938.[*] Sounds familiar, doesn't it? Today, radio (and music sales) are threatened by MP3s (driven by iPods), podcasting, web streaming, satellite radio, and mobile device streaming. Traditional radio stations no longer dominate the car, which was the primary place of use for the past several decades. With mobile phones emerging as media platforms (iPhone) and broadband speeds available over-the-air (3G+), control of audio consumption has been marginalized and user choice is now nearly unlimited.

Billboards. The out-of-home advertising industry is a little more complicated to synthesize, mainly because it's less "standardized" than the other media. It's also difficult to understand exactly when billboards started, but it certainly happened after lithography was invented, and likely took growth in the mid/late 1800s. Clear Channel is the oldest formal outdoor advertising company in the United States as their roots trace back to Foster & Kleiser, which was formed in 1901. The decrease in printing costs (think PCs and printers) over the past decade has allowed the industry to flourish from initially just outdoor billboards to wall posters, transit busboards, airport ads, shopping mall advertising, subways, taxicabs, and movie theaters. So, not only has the amount of available space (avails) increased dramatically within the industry, now billboard operators are again increasing inventory (and broadening applications) by introducing digital signage (an exponential multiplier effect). Digital signs are now seen, not only on highway billboards, but also in stores, doctors' offices, shopping malls, and gas stations at the pump! Out-of-home is a great source of lead generation for advertisers but this proliferation of choices is quite overwhelming. Advertisers seeking to reach consumers who are "on the go" today not only can choose from the dozens of aforementioned venues, but now can get listed on mobile phones coupled with mapping services or GPS navigation devices (in car or handheld).

Magazines. Last, but certainly not least, magazines, periodicals, or serials are publications, generally published on a regular schedule, containing a variety of articles, generally financed by advertising, by a purchase price, by subscriptions, or all three. With the exception of, presumably, AARP The Magazine, most magazine titles are facing declining circulation and declining ad pages, which can be a compounding problem because generally circulation drives ad rates. Magazines, by and large, are an ideal advertising medium for contextual branding (golf equipment & services in Golf Magazine or auto-related ads in Car & Driver). And, although many titles have come and gone, the magazine industry traces its roots back to familiar titles such as National Geographic and Good Housekeeping, both of which were launched in the late 1800s. Given such, over the past century, the industry has seen and survived the introduction of radio & television advertising and the evolution of newspapers & billboards. More importantly, the magazine industry itself has created fractionalization. For instance, there are twice as many titles today than a decade ago with two-thirds of the volume. The top 25 titles have been squeezed the most, their unit volume declining by one-half over the decade, only causing more choice (read: difficulty) to the advertiser. This is driven by a major shift in consumer preferences from mass to niche & special-interest titles. Ten years ago, half the volume came from the 25 largest titles; today the proportions have been reversed; almost 75% of volume comes from the several thousand smaller titles. In addition to competition from within the industry, today, magazines are also facing the same threat as the other traditional mediums, the proliferation of web content (and ad inventory) on the Internet. The proliferation & consumer adoption of mobile readers such as Kindles and multimedia devices such as the iPhone presents an entirely new set of parameters for the industry to grapple with.

And, so what's happening to the newest of the outlets:

Internet. Since the days of Netscape & AOL, the Internet has been in constant motion and continuous reinvention. The number of world wide web pages continues to grow at astronomic rates and the availability of content (blogs, books, videos, ezines, photos, etc, etc) does not appear to be slowing any time soon. To address the massive amount of insatiable inventory, hundreds of ad networks have popped up slicing & dicing viewers & advertising opportunities every which way. These ad networks, along with search engines, social networks, and "mega" content portals provide advertising an astounding amount of choice & reach. Mobile content services and online video are both relatively nascent but poised to explode and flood the market with advertising availability. These options, feeding off of tremendous growth, are also fiercely competitive, driving prices down within the Internet sector and also for the other four traditional mediums.

All of these changes, brought on by technology over the past decade plus, are creating a flood of increased ad supply in a market that historically had strong pricing power for "virtual" goods (definitely not cost-plus).

One of the overarching challenges the industry faces is one of resources on Madison Avenue. At the end of the day, enormous budgets are controlled by a relatively small number of actors who seek ease of deployment as much as they do advertising effectiveness. Also, as the Internet continues to commoditize its display ad inventory across increasingly fragmented and nameless ad networks, advertisers will need more, not fewer, places where they can count on a certain quality of content, a quality of audience, and a quality of service. Where will this put the ad rates for so-called long-tail web content? How will those rates compare to broadcast television, magazines, or audio? Will the ad market truly be efficient at pricing? Clearly, we've seen that the stock market isn't capable of it, so why should expect admen to be any more efficient?

The overarching question still holds -- is the ad market a zero sum game? Or, will the demand curve shift to meet this new supply curve? I imagine, like anything, it's likely a combination of the two.

Intellectual property piracy is a major problem facing the software and media industries today. It's always been a huge problem outside of the US and it's not becoming a much much bigger problem everywhere now that the Internet and broadband is more pervasive. Software piracy rates in places like Bangladesh and Armenia are north of ninety percent and, even in the United States, stolen software is estimated at one in five users. The Business Software Alliance regularly publishes a report on the issue.

Worldwide, roughly 41% of all software installed on personal computers is obtained illegally, with foregone revenues to the software industry totaling $53 billion.

These are staggering figures, and they only account for software. The music industry also studies the challenges. One credible analysis by the Institute for Policy Innovation concludes that global music piracy causes $12.5 billion of economic losses every year. Again, enormous figures. I've read old reports (from five years ago) that sales of bootleg music accounted for roughly 34% of all sales globally. Outside of developed markets, it would seem those numbers push well past 80-90%.

The data and staggering figures are certainly equally similar for television, video games, and film. Digital distribution, empowered by rapidly growing broadband access and pervasive mobile device internet access, is only rapidly accelerating the problem.

Industry leaders have tried various solutions to the address piracy. Software developers have tried to use "keys" as a means to control distributed copies and the music industry attempted to employ digital rights management through Apple iTunes. But, both of these attempts have largely failed to solve the problem.

As I see it, there is really only one viable solutions to intellectual property piracy. And, DRM is not it. The solution is (or almost) free content distribution with merchandising, advertising, or feature upsells. A low entry price-point (free or negligible), but peripheral monetization is how the IP industry needs to think. Zynga gives games away for free, but makes money on virtual goods. Google gives software away for free and makes money on advertising or by charging for increased storage/features. Musicians should give music away for free (or a very low cost) and monetize concerts and t-shirts. Online video should try to thrive at the intersect of nearly free (thwarting the need to pirate, yet still generating some high gross margin revenues) and monetize through volume, product placements, embedded campaigns, and interactive viewer engagement.

The net-net is that some form of hosted model with a free or cheap pricing model is a clear front-runner as a means to control piracy.

Hosted, on-demand, in-the-cloud software is one way to tackle the problem for the software industry. The drawback with that are that today (and for quite some time to come), Internet connectivity is not truly pervasive so use is somewhat confined.

The music industry has and continues to toy with various streaming, on-demand radio-like services, ranging from Napster to Pandora to Ruckus. Although not perfectly refined, they will get there eventually. Likewise, the music industry could/should look to reducing the cost of the actual music and instead monetizing the periphery (as they already do with concerts and physical products).

The gaming industry is on the forefront, with an explosion in hosted games online and online gaming communities. This industry "gets it" and is faster at exploring alternative revenue streams such as virtual goods and advertising. Piracy was a major issue in Asia, and that drove a "need" to migrate from a pay video game model to a free video game model with virtual goods. Zynga is a great case study on that model.

Video, television, and film are the least well positioned to deal with the the issue, but partnerships with Internet Service Providers can help address this. Revenue sources are bound to change (notably the syndication stream), but better customer data with targeted advertising could mean higher CPMs and product placements integrated with web strategies could provide for longer-term customer loyalty. American Idol (with interactive voting) and Heroes (with the Sprint campaign) are prime examples of the evolution of live television. The long-form film industry (excluding physical theaters) has a lot of wiggle-room in my opinion to play with pricing. A movie at the theater is $10, which is not an extraordinary sum to begin with, so with less expensive direct distribution and reasonable merchandising strategies, it would seem that the free or nearly free online showings (a la Cable On-Demand) could provide for the same bottom line.

My post clearly evolved into a lengthy, incomplete treatise that covered a lot but said little, so I'll stop here. But the thought that walk away with is that the next few years are poised to see some significant change in "soft" (video, music, software, etc) product pricing as recessions have historically accelerated structural change, and I don't expect this recession to buck that trend.

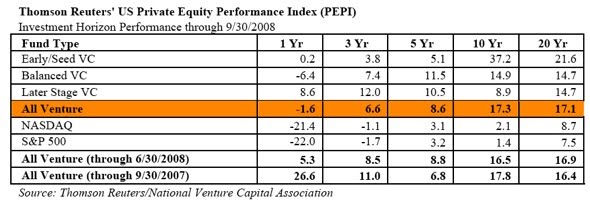

I'm fascinated by this concern that many venture capitalists (and LPs) have about 2010 catching up with the industry. Folks are concerned with plummeting ten-year venture asset-class returns. This recent article in the Wall Street Journal sums up the "problem" neatly. The following statement, I fear, is a gross over-simplification of the analysis.

The best quarter ever was the last three months of 1999 when the end-to-end return to fund investors was 83.4%. To see what is likely to happen to the 10-year return, look at the nine-year return as of June – it was minus 5.2%.While people who track venture fund returns have been expecting this, the 10-year figure is widely followed and its decline can only add to the perception that venture capital is not what it used to be.

Below are a chart from VentureBeat that highlights the issue as it's changed over the past twelve months. The trend is clearly not in the right direction.

Although I definitely agree that too many VC funds have gotten too large and that the resulting arithmetic seems unlikely and challenging, the asset class is far from broken.

This is a slight different representation of similar data.

Asset managers can pick from a variety of different asset classes, and portfolio theory tells us that we should diversify. However, had I not invested in the venture asset class ten years ago, and instead invested in the major equity indices, I would not be better off. Below is the NASDAQ performance over exactly the past 10 years.

And, here is the performance of the Dow Jones Industrial Average, the S&P 500, and the NASDAQ on a different scale.

How can you tell me that the venture asset class is broken without providing an alternative? Performance is relative, unfortunately some might say, so looking at one product's performance in isolation is not an appropriate way to evaluate a portfolio strategy.

More importantly, as it relates to the venture capital asset class, at the end of the day, it's very much a cottage industry run by human beings who manage different strategies and investment tactics. When evaluating venture capital performance, interesting data might be to better understand how fund size over the past ten years has affected returns and likewise geographic focus has affected performance. Other evaluation criteria could/should include sector focus as well (life sciences versus software versus clean tech, etc). I bet that several of these three criteria have as much to do with performance as vintage year, just as capitalization (size; large cap, small cap, etc) and industry (industrials, technology, healthcare, etc) impact public equity indices differently.

A review of ideas, thoughts, rants, raves, and other musings from a young entrepreneur, venture capitalist, technology analyst, globalisation pundit, relationship developer, and kiteboarding fanatic.

About

A citizen of the world living in NY, but following business, technology, finance, and life around the globe, you can find out a little more about me here.

Feel free to drop me a note or phone call, I always welcome a good conversation, a challenging squash game, a new deal, or a glass of great wine.

But, the question to ponder is whether the market will evolve as Macintosh and Windows did or whether Apple will hold ground & continue to grow. Will, over time, the Mobile OS world sustain multiple providers or will we end up in a world where one OS dominates market share?

Is there a developer, application, and user network effect in the mobile world? Any kind of network effect could impact this outcome uniquely.

On the face of things, it would seem to me that Google is taking a page from the Microsoft Windows playbook and Apple is taking a page from, well, the, uh, not so successful Apple Macintosh playbook.

It could also just be that the Mobile OS world can end up looking very much like the video game console industry, with three players (Microsoft XBox, Sony PlayStation, & Nintendo Wii) today equally vying for market share along with several other players (Sega, Atari, 3DO, NEC, RCA, etc) making waves here & there.

What about RIM, Nokia, Motorola, and Symbian in this above discussion? And, dare I say, Palm? Is it sound to simply assume that these players are out of the running?

Although more free market examples would imply a standard Google & Microsoft analogy, only time will tell how the Mobile OS world evolves differently. As mobile applications become more complex, 3G connectivity becomes more pervasive, and devices become more powerful, the Mobile OS landscape will also become more expensive to compete in. For now, though, my guess is that it's still pretty early to start predicting the next Windows.